1. What is a derivative, and how is it used in financial markets?

A derivative is a financial instrument whose value is derived from the value of an underlying asset. The underlying asset can be a variety of things including stocks, bonds, commodities, currencies, interest rates, or market indexes. The main types of derivatives include forward contracts, futures contracts, options, and swaps. Derivatives are commonly used for hedging risk, speculation, and arbitrage purposes.

2. Can you explain the different types of derivatives?

Forward Contracts: A forward contract is a customized agreement between two parties to buy or sell an asset at a specified price on a future date. These contracts are traded over-the-counter (OTC) meaning they are not standardized or traded on exchanges.

Futures Contracts: A futures contract is a standardized agreement to buy or sell an asset at a specified price on a future date. These contracts are traded on exchanges, which provide standardization and liquidity.

Options: An option is a contract that gives the holder the right, but not the obligation, to buy (call option) or sell (put option) an underlying asset at a specified price (strike price) before or at a specified expiration date.

Swaps: A swap is a derivative contract through which two parties exchange financial instruments, typically cash flows based on predefined terms. The most common types are interest rate swaps and currency swaps.

3. What are the specifications mentioned in a derivative contract?

Here are the specifications commonly mentioned in a derivative contract:

Underlying Asset: The specific asset, index, or rate upon which the derivative contract is based (e.g., a stock, commodity, currency, or interest rate)

Contract Type: The type of derivative (e.g., forward, futures, option, or swap).

Contract Size: The quantity or amount of the underlying asset that the contract represents (e.g., 100 shares of a stock, 1,000 barrels of oil).

Price/Strike Price: The agreed-upon price at which the underlying asset will be bought or sold (in options, this is known as the strike price).

Expiration Date: The date on which the derivative contract expires and the final settlement occurs.

Settlement Terms: The method of settlement, which can be either physical delivery of the underlying asset or settlement based on the underlying asset’s value at expiration.

Margin Requirements: The amount of collateral required to enter into and maintain the position (applicable primarily to futures contracts and options).

Premium: For options, the premium is the price paid by the buyer to the seller for the option contract.

Exercise Terms: For options, the conditions under which the option can be exercised (e.g., American options can be exercised any time before expiration, while European options can only be exercised at expiration).

Counterparties: The identities of the parties involved in the contract.

Notional Amount: In swaps and some other derivatives, the notional amount is the face value on which the exchange of payments is based.

Payment Terms: The schedule and calculation method for any payments to be made under the contract (e.g., interest payments in a swap agreement).

Clearing and Settlement: For exchange-traded derivatives, details of the clearinghouse involved and the clearing process.

Early Termination Provisions: Conditions under which the contract can be terminated early by either party.

Collateral Requirements: The collateral that must be posted by the parties to mitigate counterparty risk.

Additional Terms and Conditions: Any other specific terms or conditions that apply to the contract, such as triggers for default or specific events that affect the contract’s execution.

4. What is exchange-traded markets, and can you describe their key characteristics?

Exchange-traded markets are financial markets where standardized contracts for various financial instruments, such as derivatives, stocks, bonds, and commodities, are bought and sold. These markets are centralized platforms, typically operated by exchanges, where buyers and sellers meet to trade these financial instruments.

Key Characteristics of Exchange-Traded Markets:

Standardization: Contracts traded on exchange-traded markets are standardized in terms of quantity, quality, and delivery time. This standardization ensures that all contracts are uniform and interchangeable.

Transparency: Exchange-traded markets offer high levels of transparency. Information about prices, trading volumes, and other relevant data is readily available to all market participants.

Liquidity: Due to the centralized nature and large number of participants, exchange-traded markets tend to have high liquidity, making it easier for traders to enter and exit positions without significantly affecting prices.

Regulation: Exchanges are subject to regulatory oversight by governmental and other regulatory bodies, which helps ensure fair trading practices and reduces the risk of fraud and manipulation.

Counterparty Risk: Exchanges typically have clearinghouses that act as intermediaries between buyers and sellers, ensuring that transactions are completed smoothly and less counterparty risk.

5. What are over-the-counter (OTC), and can you describe their key characteristics?

Over-the-counter (OTC) are decentralized markets where financial instruments such as stocks, bonds, currencies, and derivatives are traded directly between two parties without the oversight of an exchange. These markets operate through a network of dealers and brokers who negotiate directly with each other, often over the phone or via electronic systems.

Key Characteristics of OTC:

Decentralization: OTC do not have a centralized exchange or physical location. Trading takes place directly between parties, often through electronic communication networks or over the phone.

Customization: Contracts traded in OTC can be highly customized to meet the specific needs of the parties involved. This allows for greater flexibility in terms, such as contract size, expiration date, and underlying assets.

Lack of Transparency: OTC are less transparent than exchange-traded markets because trades are not always publicly reported. This can make it harder to determine market prices and trading volumes.

Liquidity: Liquidity in the OTC (over-the-counter) is generally lower compared to exchange-traded derivatives because transactions are negotiated privately between parties, leading to less transparency and fewer participants.

Regulation: OTC are generally less regulated than exchange-traded markets. However, they are still subject to oversight by regulatory bodies to some extent, depending on the jurisdiction and the specific market.

Counterparty Risk: Because OTC trades are conducted directly between parties without an intermediary, there is a higher risk of counterparty default. This risk can be mitigated through credit arrangements or collateral agreements.

|

Feature |

Forward Contracts |

Futures Contracts |

|

Trading Venue |

Over-the-counter (OTC) |

Traded on organized exchanges |

|

Standardization |

Customized terms (size, expiration, etc.) |

Standardized terms (size, expiration, etc.) |

|

Counterparty Risk |

Higher counterparty risk (no clearinghouse) |

Lower counterparty risk (clearinghouse guarantees) |

|

Regulation |

Less regulated |

Highly regulated |

|

Settlement |

Settled at maturity |

Daily settlement (marked-to-market) |

|

Margin Requirements |

Typically, no margin requirements |

Initial and maintenance margins required |

|

Liquidity |

Generally, less liquid due to customization |

Generally, more liquid due to standardization |

|

Transparency |

Less transparent (private negotiation) |

Highly transparent (publicly available prices and volumes) |

|

Contract Flexibility |

Highly flexible to meet specific needs of parties |

Less flexible due to standardization |

|

Delivery |

Usually settled by physical delivery |

Can be settled by physical delivery or cash settlement |

|

Pricing |

Priced based on the agreed terms between the parties |

Priced based on market conditions and standardized terms |

|

Use Case Examples |

Hedging as per specific needs |

Speculation, hedging, and arbitrage on standardized terms |

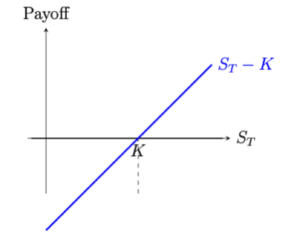

7. Can you draw the payoff for a forward contract for both the long and short positions?

Payoff from a Long Forward Position A long position in a forward contract has the following payoff at maturity:

where S_T is the underlying asset’s price at maturity, and K is the forward price agreed upon when entering the contract.

where S_T is the underlying asset’s price at maturity, and K is the forward price agreed upon when entering the contract.

When S_T = K, the payoff is zero. If S_T rises above K, the long position gains (positive payoff). If S_T < K, the payoff is negative.

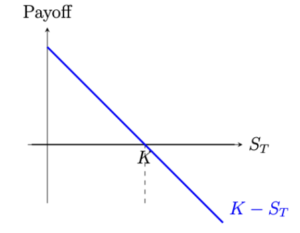

Payoff from a Short Forward Position A short position in a forward contract has the following payoff at maturity:

When S_T = K, the payoff is zero. If S_T falls below K, the short position gains (positive payoff). If S_T > K, the payoff is negative.

When S_T = K, the payoff is zero. If S_T falls below K, the short position gains (positive payoff). If S_T > K, the payoff is negative.

8. Can you draw the payoff for a futures contract for both the long and short positions?

Payoff from a Long Futures Position

A long futures position effectively has the following value at expiration:

![]()

where S_T is the price of the underlying at maturity (expiration), and F_0 is the agreed-upon futures price when the contract was initiated. (The key difference from a forward is the daily settlement, but the final net payoff at expiration is the same.)

When S_T = F_0, the position’s net value is zero at expiration. If S_T > F_0, the long futures holder gains. If S_T < F_0, the payoff is negative.

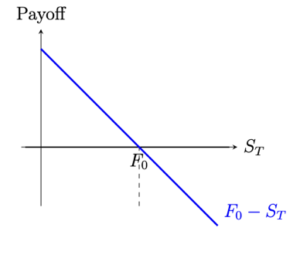

Payoff from a Short Futures Position

A short futures position has this value at expiration:

![]() When S_T = F_0, the short futures position’s net value is zero at expiration. If S_T < F_0, the short futures holder gains. If S_T > F_0, the payoff is negative.

When S_T = F_0, the short futures position’s net value is zero at expiration. If S_T < F_0, the short futures holder gains. If S_T > F_0, the payoff is negative.

Note: Despite daily marking-to-market in futures, the final net payoff at the contract’s expiration matches these simple linear formulas, just as with forward contracts. The difference is that gains or losses are realized (and credited/debited) day by day, rather than only at the end.

Note: Despite daily marking-to-market in futures, the final net payoff at the contract’s expiration matches these simple linear formulas, just as with forward contracts. The difference is that gains or losses are realized (and credited/debited) day by day, rather than only at the end.

9. What is a Hedger, Arbitrageur and Speculator?

Hedger: A hedger is a market participant who uses derivatives or other financial instruments to mitigate the risk of adverse price movements in an underlying asset. The primary objective of hedging is to protect against potential losses rather than to make a profit.

Arbitrageur: An arbitrageur is a trader who seeks to profit from price discrepancies of the same or similar financial instruments in different markets or forms. Arbitrageurs exploit these discrepancies by simultaneously buying and selling the asset to achieve a risk-free profit.

Speculator: A speculator is a market participant who takes on risk by trading financial instruments with the aim of making a profit from anticipated price movements. Speculators do not seek to hedge risks or exploit arbitrage opportunities; instead, they bet on future price changes.

10. How are future contracts used in hedging, arbitrage and speculation?

Futures contracts can be used in hedging, arbitrage, and speculation in various ways. Here’s how they are applied in each context:

Hedging:

A wheat farmer expects to harvest 100,000 bushels of wheat in six months. The current market price of wheat is $5 per bushel, but the farmer is concerned that the price might fall by the time of harvest.

- Action: The farmer sells wheat futures contracts to lock in the price of $5 per bushel for the future delivery.

- Outcome: If the market price of wheat falls to $4 per bushel at harvest, the farmer still receives $5 per bushel through the futures contract, thus hedging against the price decline. Conversely, if the price rises to $6 per bushel, the farmer benefits less but has ensured a stable income.

Arbitrage:

An arbitrageur notices that the price of gold futures on one exchange is $1,800 per ounce, while on another exchange it is $1,805 per ounce.

- Action: The arbitrageur buys gold futures at $1,800 per ounce on the first exchange and simultaneously sells gold futures at $1,805 per ounce on the second exchange.

- Outcome: The arbitrageur locks in a risk-free profit of $5 per ounce, exploiting the price discrepancy between the two exchanges.

Speculation:

A trader believes that the price of oil, currently at $60 per barrel, will rise significantly in the next three months.

- Action: The trader buys oil futures contracts at $60 per barrel.

- Outcome: If the price of oil rises to $70 per barrel, the trader can sell the futures contracts at the higher price, making a profit of $10 per barrel. Conversely, if the price falls to $50 per barrel, the trader incurs a loss of $10 per barrel.

In futures trading, margin requirements are essential to ensure that both parties involved in the contract can fulfill their financial obligations. Margin requirements help manage the risk of default by providing a financial buffer. Here are the key aspects of margin requirements in futures contracts:

Types of Margins

Initial Margin: The initial margin is the amount of money required to open a futures position. It is a fraction of the total contract value and acts as a good-faith deposit. Generally, the initial margin is between 2 to 12 percent of the future contract (depending on the specification of the contract).

Maintenance Margin: The maintenance margin is the minimum amount of money that must be maintained in a margin account to keep a futures position open.

Margin Call: A margin call occurs when the account balance falls below the maintenance margin requirement. The trader must deposit additional funds to bring the account back to the initial margin level.

Variation Margin: The amount deposited to bring the account back up to the initial margin level is called the variation margin.

12. How Margin Requirements work? Give an example of margin requirements.

Opening a Position: When a trader opens a futures position, they must deposit the initial margin into their margin account. This acts as collateral to cover potential losses.

Daily Settlement: Futures contracts are marked-to-market daily. This means that gains and losses are realized at the end of each trading day and are credited or debited to the trader’s margin account.

Margin Calls: If daily losses reduce the account balance below the maintenance margin, the trader receives a margin call and must deposit additional funds to meet the initial margin requirement.

Closing a Position: When a trader closes a futures position, any remaining margin in the account, adjusted for gains or losses, is returned to the trader.

Example of Margin Requirements:

Opening the Position:

- A trader buys a futures contract for 1,000 barrels of oil at $60 per barrel. The total contract value is $60,000.

- The initial margin requirement is 10 percent, so the trader must deposit $6,000 and maintenance margin is 7 percent.

Daily Mark-to-Market:

- If the price of oil rises to $62 per barrel the next day, the contract’s value increases to $62,000.

- The trader’s account is credited with the gain of $2,000, bringing the margin account balance to $8,000 ($6,000 + $2,000).

Margin Call:

- If the price of oil falls to $58 per barrel the following day, the contract’s value decreases to $58,000.

- The trader’s account is debited with the loss of $2,000, bringing the margin account balance to $4,000 ($8,000 – $4,000).

- Since $4,000 is below the $4,200 maintenance margin (7 percent of $60,000), a margin call is issued. The trader must deposit $2,000 to bring the account back to the initial margin level of $6,000. The $2,000 is called as a variation margin.