1. What are Options? Explain its types?

Options are financial derivatives that provide the holder with the right, but not the obligation, to buy or sell an underlying asset at a predetermined price (known as the strike price) at a predetermined date. They are used for various purposes, including hedging risk, speculation, and generating income.

Key Types of Options

Call Options: A call option gives the holder the right to buy the underlying asset at a predetermined price (known as the strike price) at a predetermined date.

Put Options: A put option gives the holder the right to sell the underlying asset at the strike price before or at the expiration date.

2. Can you give an example of how Options work?

Call Option:

An investor buys a call option on XYZ stock with:

- Strike Price: $50

- Expiration: 3 months

- Premium Paid: $5

If the stock price rises to $60 before expiration:

- The investor can exercise the option to buy the stock at $50.

- Profit Calculation: $10 per share (sale at $60 – buy at $50) – $5 premium = $5 net profit per share.

If the stock price does not exceed $50:

- The option expires worthless.

- Loss: Investor loses the $5 premium paid.

Put Option:

An investor buys a put option on ABC stock with:

- Strike Price: $50

- Expiration: 3 months

- Premium Paid: $5

If the stock price falls to $40 before expiration:

- The investor can exercise the option to sell the stock at $50.

- Profit Calculation: $10 per share (sale at $50 – market price at $40) – $5 premium = $5 net profit per share.

If the stock price does not fall below $50:

- The option expires worthless.

- Loss: Investor loses the $5 premium paid.

3. What are different positions an investor can take in an Option?

An investor can take the following positions:

- Long Call: Buying a call option, giving the holder the right to buy the underlying asset at a specified price, expecting the asset’s price to rise.

- Long Put: Buying a put option, giving the holder the right to sell the underlying asset at a specified price, expecting the asset’s price to fall.

- Short Call: Selling a call option, obligating the seller to sell the asset if the buyer exercises the option, expecting the asset’s price to stay the same or fall.

- Short Put: Selling a put option, obligating the seller to buy the asset if the buyer exercises the option, expecting the asset’s price to stay the same or rise.

Note: When you are in a long position, you need to pay the premium and when you are in short position, you receive the premium. Remember that the keyword “long” means to buy and “short” means to sell.

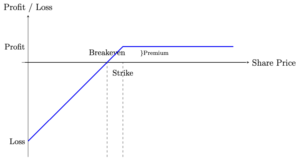

4. What is a Long Call Option?

A long call option is a financial position in which an investor buys a call option, giving them the right, but not the obligation, to buy a specified amount of an underlying asset at a predetermined strike price at a predetermined date.

This position is typically taken when the investor expects the price of the underlying asset to rise.

Key Features of a Long Call:

- Right to Buy: The holder has the right to purchase the underlying asset at the strike price.

- Premium: The holder pays a premium to acquire the call option.

- Potential for Unlimited Profit: The potential profit is unlimited if the price of the underlying asset rises significantly above the strike price.

- Limited Loss: The maximum loss is limited to the premium paid for the option.

Where:

- S is the price of the underlying asset at expiration.

- K is the strike price of the option.

- P is the premium paid for the option.

Example:

Suppose an investor buys a call option on a stock with the following details:

- Strike Price (K): $50

- Premium (P): $5

- Expiration: 3 months

If the stock price at expiration (S) is $60:

- Payoff = max(0, 60 – 50) = 10

- Profit = 10 – 5 = 5

If the stock price at expiration (S) is $45:

- Payoff = max(0, 45 – 50) = 0

- Profit = 0 – 5 = -5

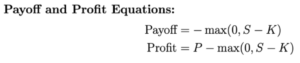

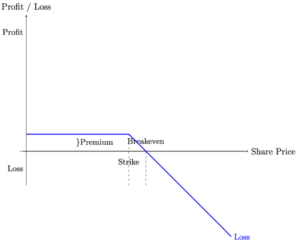

5. What is a Short Call Option?

A short call option position involves selling a call option, giving the seller (also known as the writer) the obligation to sell the underlying asset at the predetermined price (strike price) if the option is exercised by the buyer.

The seller receives a premium for taking on this obligation. This position is typically taken when the seller expects the price of the underlying asset to remain below the strike price or decrease.

Key Features of a Short Call:

- Obligation to Sell: The writer has the obligation to sell the underlying asset at the strike price if the buyer exercises the option.

- Premium Income: The writer receives a premium for selling the call option, which is the maximum profit potential.

- Potential for Unlimited Loss: If the price of the underlying asset rises significantly above the strike price, the potential loss is unlimited.

- Limited Profit: The maximum profit is limited to the premium received for selling the call option.

Where:

- K is the strike price of the option.

- S is the price of the underlying asset at expiration.

- P is the premium received for the option.

Example:

Example:

Suppose an investor sells a call option on a stock with the following details:

- Strike Price (K): $50

- Premium Received (P): $5

- Expiration: 3 months

If the stock price at expiration (S) is $60:

- Payoff = -max(0, 60 – 50) = -10

- Profit = 5 – 10 = -5

If the stock price at expiration (S) is $45:

- Payoff = -max(0, 45 – 50) = 0

- Profit = 5 – 0 = 5

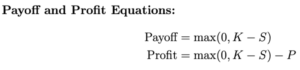

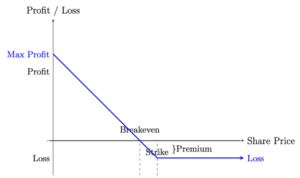

6. What is a Long Put Option?

A long put option position involves buying a put option, which gives the holder the right, but not the obligation, to sell the underlying asset at a predetermined strike price and at a predetermined date.

This position is typically taken when the investor expects the price of the underlying asset to decline.

Key Features of a Long Put:

- Right to Sell: The holder has the right to sell the underlying asset at the strike price.

- Premium Payment: The holder pays a premium to acquire the put option.

- Potential for Significant Profit: The potential profit is substantial if the price of the underlying asset falls significantly below the strike price.

- Limited Loss: The maximum loss is limited to the premium paid for the option.

Where:

Where:

- K is the strike price of the option.

- S is the price of the underlying asset at expiration.

- P is the premium paid for the option.

Example:

Example:

Suppose an investor buys a put option on a stock with the following details:

- Strike Price (K): $50

- Premium Paid (P): $5

- Expiration: 3 months

If the stock price at expiration (S) is $40:

- Payoff = max(0, 50 – 40) = 10

- Profit = 10 – 5 = 5

If the stock price at expiration (S) is $55:

- Payoff = max(0, 50 – 55) = 0

- Profit = 0 – 5 = -5

7. What is a Short Put Option?

A short put option position involves selling a put option, giving the seller (also known as the writer) the obligation to buy the underlying asset at the strike price if the option is exercised by the buyer. The seller receives a premium for taking on this obligation.

This position is typically taken when the seller expects the price of the underlying asset to remain above the strike price or increase.

Key Features of a Short Put:

- Obligation to Buy: The writer has the obligation to purchase the underlying asset at the strike price if the buyer exercises the option.

- Premium Income: The writer receives a premium for selling the put option, which is the maximum profit potential.

- Potential for Significant Loss: If the price of the underlying asset falls significantly below the strike price, the potential loss can be substantial.

- Limited Profit: The maximum profit is limited to the premium received for selling the put option.

Where:

- K is the strike price of the option.

- S is the price of the underlying asset at expiration.

- P is the premium received for the option.

Example:

Suppose an investor sells a put option on a stock with the following details:

- Strike Price (K): $50

- Premium Received (P): $5

- Expiration: 3 months

If the stock price at expiration (S) is $55:

- Payoff = -max(0, 50 – 55) = 0

- Profit = 5 – 0 = 5

If the stock price at expiration (S) is $40:

- Payoff = -max(0, 50 – 40) = -10

- Profit = 5 – 10 = -5

8. What factors affect the price of the Option?

Following are the factors that affect the price of an option:

- Stock price

- Strike price

- Time to expiry

- Volatility

- Risk-free interest rate

- Dividend

- Supply & Demand

9. What is the difference between American and European options?

American and European options are two types of options contracts that differ mainly in terms of when the options can be exercised.

American Options:

- Exercise: Can be exercised at any time before and including the expiration date.

- Flexibility: Provides greater flexibility to the holder, as they can choose the optimal time to exercise based on market conditions.

- Common Use: Typically used for options on individual stocks and commodities.

European Options:

- Exercise: Can only be exercised on the expiration date.

- Predictability: Provides less flexibility but simplifies valuation and hedging strategies because the exercise date is fixed.

- Common Use: Often used for options on indices and certain financial derivatives.

10. Define moneyness of the Option?

Moneyness is a term used to describe the relationship between the price of the underlying asset and the strike price of an option. It indicates whether exercising the option would be profitable if it were exercised right now. Moneyness helps traders and investors understand the intrinsic value of an option.

In-the-Money (ITM):

- Call Option: A call option is in-the-money if the price of the underlying asset (S) is greater than the strike price (K). S > K

- Put Option: A put option is in-the-money if the price of the underlying asset (S) is less than the strike price (K). S < K

At-the-Money (ATM):

- Call and Put Options: An option is at-the-money if the price of the underlying asset (S) is equal to the strike price (K). S = K

Out-of-the-Money (OTM):

- Call Option: A call option is out-of-the-money if the price of the underlying asset (S) is less than the strike price (K). S < K

- Put Option: A put option is out-of-the-money if the price of the underlying asset (S) is greater than the strike price (K). S > K

11. Can you explain the concepts of intrinsic and extrinsic value in options, and how these are determined?

Understanding the intrinsic and extrinsic values of options is crucial for assessing their overall worth and making informed trading decisions.

Intrinsic Value:

Intrinsic value is the inherent value of an option if it were exercised immediately. It is determined by the difference between the underlying asset’s current price and the option’s strike price. Intrinsic value reflects the profit that would be realized if the option were exercised at the current moment.

- Call Option: The intrinsic value of a call option is calculated as:

Intrinsic Value = max(0, S – K)

- Put Option: The intrinsic value of a put option is calculated as:

Intrinsic Value = max(0, K – S)

Extrinsic Value:

Extrinsic value is also known as “time value” because the time left until the option contract expires is one of the primary factors affecting the Extrinsic Value. Another factor that affects the extrinsic value is Implied Volatility.

Extrinsic Value = Option Premium – Intrinsic Value

The option premium is the total price of the option.

Understanding the intrinsic and extrinsic values helps traders and investors assess the true worth of an option and make informed decisions about buying, selling, or holding options based on their market expectations and risk tolerance.

12. What are the advantage and disadvantage of trading In-the-Money (ITM) Options?

Advantages:

- Higher Intrinsic Value: ITM options have intrinsic value because the strike price is favorable compared to the current price of the underlying asset.

- Greater Likelihood of Profit: Since ITM options already have intrinsic value, they are more likely to be exercised or sold at a profit compared to at-the-money (ATM) or out-of-the-money (OTM) options.

- Lower Risk of Expiration Worthless: ITM options have less risk of expiring worthless compared to OTM options because the underlying asset price is already in a favorable range for the option holder.

Disadvantages:

- Higher Premium: ITM options are more expensive than OTM or ATM options because they have intrinsic value. The higher premium means a larger upfront cost to enter the trade.

- Less Leverage: Compared to OTM options, ITM options provide less leverage, as a significant portion of their price is intrinsic value. This means the potential for large percentage gains (if the underlying asset moves favorably) is reduced compared to OTM options.

- Limited Upside in Volatile Markets: ITM options may not benefit as much from increases in volatility compared to OTM options, which are more sensitive to changes in implied volatility and time value.

13. What are the advantage and disadvantage of trading At-the-Money (ATM) Options?

Advantages:

- Balanced Premium: ATM options typically have a moderate premium, combining both intrinsic value (which is close to zero) and extrinsic value, making them less expensive than ITM options but more affordable than OTM options.

- High Sensitivity to Price Movement: ATM options are highly responsive to changes in the price of the underlying asset. Small movements can significantly affect the option’s value, offering a good balance between risk and reward.

- Best for Gamma and Theta: ATM options benefit from having the highest gamma (rate of change of delta) and theta (time decay) values, making them ideal for short-term strategies and capturing quick price movements.

Disadvantages:

- Can Expire Worthless: If the underlying asset price does not move beyond the strike price, the ATM option can expire worthless, meaning the buyer loses the entire premium paid.

- Time Decay is Fast: As ATM options approach expiration, the extrinsic value decays rapidly due to time decay (theta), leading to a loss of value if the underlying asset doesn’t move significantly.

- Uncertainty: ATM options are at a critical point where the underlying asset’s price is close to the strike price, adding uncertainty. The position can easily become OTM or ITM with small price movements.

14. What are the advantage and disadvantage of trading Out-of-the-Money (OTM) Options?

Advantages:

- Lower Premium: OTM options have lower premiums because they have no intrinsic value. This makes them a cost-effective way to take a position with limited initial investment.

- High Leverage Potential: OTM options offer the highest leverage. If the underlying asset’s price moves significantly in the right direction, the percentage gain can be substantial, potentially offering high rewards relative to the premium paid.

- Best for Speculation: OTM options are favored by speculators due to their low cost and high potential for profit if the underlying asset experiences large price swings.

Disadvantages:

- Higher Risk of Expiring Worthless: OTM options have no intrinsic value at the time of purchase, meaning they are more likely to expire worthless if the underlying asset’s price doesn’t move in the expected direction.

- Time Decay: OTM options lose their value quickly as time passes, especially close to expiration. Since their value is entirely based on extrinsic factors, time decay can quickly erode the option’s value if the underlying asset doesn’t move in favor of the option holder.

- Lower Probability of Profit: OTM options have a lower probability of reaching the strike price, meaning the chances of realizing a profit are smaller compared to ITM or ATM options.

15. What are different types of underlying in an option contract?

Here are the different types of underlying assets in options contracts:

- Stocks (Equities): Options on individual company stocks give the right to buy or sell shares at a specific price. For instance, you can trade options on shares of companies like Apple (AAPL), Microsoft (MSFT), or Tesla (TSLA).

- Indexes: Index options are based on a stock market index, which is a composite of multiple stocks representing a specific market segment. Examples include options on the SP 500 (SPX), NASDAQ-100 (NDX), or Dow Jones Industrial Average (DJX).

- Exchange-Traded Funds (ETFs): Options on ETFs represent a basket of assets, often tracking an index, sector, commodity, or other asset classes. Examples are options on SPDR SP 500 ETF (SPY), Invesco QQQ ETF (QQQ), or iShares Russell 2000 ETF (IWM).

- Currencies: Options on currencies involve trading the right to exchange one currency for another at a specified rate. Examples include options on currency pairs like EUR/USD, GBP/USD, or USD/JPY.

- Commodities: Options on physical commodities allow traders to buy or sell a specific amount of a commodity at a predetermined price. Examples are options on gold, oil, silver, or agricultural products like wheat or corn.

- Interest Rates: Options on interest rates are based on underlying financial instruments such as bonds or interest rate futures. Examples include options on U.S. Treasury bonds or Eurodollar futures.

- Futures Contracts: Options on futures give the right to buy or sell a futures contract at a specific price. Examples include options on futures for crude oil, natural gas, or stock index futures like the SP 500 futures.

- Real Estate Investment Trusts (REITs): Options on REITs represent the right to buy or sell shares in a company that owns and operates income-generating real estate. Examples include options on companies like American Tower Corporation (AMT) or Simon Property Group (SPG).

- Mutual Funds: While less common, there are options based on mutual funds that give the right to buy or sell shares in a mutual fund. Examples are specific mutual fund shares, though these are less frequently traded compared to ETFs.

- Volatility Indexes: Options on volatility indexes are based on the implied volatility of market index options. A prime example is options on the CBOE Volatility Index (VIX).

16. Can you explain different types of orders placed by Trader in the Future Market?

Here are the different types of orders placed by traders in the futures market:

Market Order: A market order is used to buy or sell a futures contract immediately at the current market price. Traders use market orders when they need to enter or exit a position quickly, regardless of the exact price, ensuring the order is executed immediately.

Limit Order: A limit order specifies a price at which a trader is willing to buy or sell a futures contract. For buy orders, it is at the limit price or lower; for sell orders, it is at the limit price or higher. Traders use limit orders to control the execution price, accepting the risk that the order may not be filled if the market does not reach the specified price.

Stop Order (Stop-Loss Order): A stop order becomes a market order once the market reaches a specified price, known as the stop price. Traders use stop orders to limit losses or protect profits on an existing position by triggering an order to buy or sell when the market moves unfavorably.

Stop-Limit Order: A stop-limit order combines features of stop and limit orders. Once the stop price is reached, the order becomes a limit order to buy or sell at a specified price or better. Traders use stop-limit orders to gain more control over the execution price after the stop price is triggered, reducing the risk of getting an unfavorable price.

Good-Till-Canceled (GTC) Order: A GTC order remains active until it is either executed or manually canceled by the trader. Traders use GTC orders when they want their order to stay open across multiple trading sessions until their specified conditions are met.

Day Order: A day order is only valid for the trading day on which it is placed. If it is not executed by the end of the trading session, it is automatically canceled. Traders use day orders when they do not want their orders to carry over to the next trading day.

17. What is Put-Call Parity?

Put-Call Parity is a fundamental principle in options pricing that defines a specific relationship between the prices of European put and call options with the same strike price and expiration date.

This principle helps in understanding how call and put options are interrelated and ensures that there are no arbitrage opportunities in the market. The equation is given by:

where C is the call option price, P is the put option price, S is the current stock price, K is the strike price, r is the risk-free interest rate, and T is the time to expiration.

18. What are the assumptions underlying the Put-Call Parity principle?

The Put-Call Parity principle is based on the following key assumptions:

(a) European Options: The put-call parity applies to European options, which can only be exercised at expiration.

(b) No Dividends: The underlying asset does not pay dividends during the life of the options.

(c) Efficient Markets: The market is efficient, meaning that all available information is reflected in the prices of securities and options.

(d) No Transaction Costs: There are no transaction costs, taxes, or fees for buying or selling options or the underlying asset.

(e) Constant Interest Rates: The risk-free interest rate is constant over the life of the options.

(f) No Arbitrage Opportunities: The market does not allow for arbitrage opportunities, meaning that it is impossible to make a risk-free profit by exploiting price differences.

19. How would you derive the Put-Call Parity equation?

The put-call parity establishes a relationship between the prices of a European call option, a European put option, and the underlying asset.

Step 1: Set up two portfolios

Portfolio A:

- Long European call option (C).

- Long a zero-coupon bond with a face value of K, maturing at time T. The bond’s current price is Ke^(-rT), where r is the risk-free interest rate and T is the time to expiration.

Portfolio B:

- Long European put option (P).

- Long one share of the underlying asset (S).

Step 2: Determine the payoffs at expiration

Portfolio A: (Call option + Bond)

Portfolio B: (Put option + Underlying asset)

Step 3: Equate the portfolios

Step 3: Equate the portfolios

Since the payoffs at expiration are identical, the cost of setting up both portfolios today must be the same to avoid arbitrage opportunities:

Step 4: Rearrange the equation

To derive the put-call parity equation, we can rearrange the terms:

This is the put-call parity formula, which shows the relationship between the prices of European call and put options, the underlying asset, and a zero-coupon bond that matures at the strike price.

20. Why is Put-Call Parity important in options pricing?

Put-Call Parity is important because it ensures that there are no arbitrage opportunities in the options market. If the relationship does not hold, traders can potentially make risk-free profits by exploiting the price differences between puts, calls, and the underlying asset.

Importance of Put-Call Parity:

(a) Ensures No Arbitrage Opportunities: Put-Call Parity ensures that the prices of options are consistent with each other and with the price of the underlying asset. If this relationship does not hold, arbitrageurs can create risk-free portfolios to profit from the discrepancies.

(b) Provides a Pricing Benchmark: The Put-Call Parity relationship provides a benchmark for the pricing of options. Traders and market participants use this relationship to verify that the prices of options are in line with the theoretical values.

(c) Helps in Understanding Market Sentiment: By analyzing deviations from Put-Call Parity, traders can gain insights into market sentiment and expectations.

21. How can Put-Call Parity be used to identify arbitrage opportunities?

If the Put-Call Parity equation is violated, arbitrage opportunities arise. For example, if

an arbitrageur can simultaneously buy the undervalued option and sell the overvalued option, along with taking appropriate positions in the stock and risk-free bonds, to lock in a risk-free profit.

22. How can Put-Call Parity be adjusted for options on assets with dividends?

Put-Call Parity for Dividend-Paying Assets

When the underlying asset pays dividends, the traditional put-call parity must be adjusted to account for the impact of those dividends on the asset’s price. Dividends reduce the price of the underlying asset, which in turn affects the value of both the call and put options.

The adjusted put-call parity formula is:

Where:

- C = Price of the European call option

- P = Price of the European put option

- S = Current price of the underlying asset

- D = Present value of dividends paid during the life of the option

- K = Strike price of the option

- r = Risk-free interest rate

- T = Time to expiration (in years)

Key Adjustments

Present Value of Dividends (D): The adjustment to the put-call parity accounts for the dividends paid during the life of the option. Since dividends reduce the price of the underlying asset, we subtract the present value of expected dividends (D) from the asset’s current price (S) to reflect the true value of the underlying asset to the option holder.

Explanation

Dividends impact the pricing of both call and put options because they cause the price of the underlying asset to drop by the dividend amount on the ex-dividend date.

- For Call Options: The call option holder does not receive dividends. Therefore, the call option becomes slightly less valuable, as the stock price is expected to drop due to dividend payments, reducing the likelihood of a large price increase.

- For Put Options: Put options may increase in value, as the underlying asset’s price is expected to decline due to dividends. This makes it more likely that the put option will finish in the money.

In summary, the adjustment to put-call parity for dividend-paying assets accounts for the reduced price of the underlying asset due to dividend payments. This ensures that the parity relationship accurately reflects the effects of dividends on option pricing.

23. How does the Put-Call Parity change if the options are American instead of European?

For European options, the put-call parity relationship is strict. However, for American options, which can be exercised at any time before or on expiration, the put-call parity relationship is expressed as an inequality due to the possibility of early exercise.

American Put-Call Parity Inequality

Where:

- C_A = Price of the American call option

- P_A = Price of the American put option

- S = Current price of the underlying asset

- K = Strike price

- r = Risk-free interest rate

- T = Time to expiration

Explanation

Key Differences from European Put-Call Parity

- Early Exercise: American options can be exercised before expiration, which can affect their pricing, especially for dividend-paying stocks. Hence, the put-call parity is expressed as an inequality.

- Range of Values: Instead of a strict equality, American put-call parity gives a range of values for the relationship between call and put prices.